Product strategy & building right to win in any market

Lessons from Niyo's delightful user onboarding

Product strategy is creating (maximum) user delight in hard to compete margin enhancing ways - Gibson Biddle(ex-Netflix/Chegg)

Table of contents

Why technology matters for vertical businesses and how the market prices them ?

No one gets fired for picking IBM - building an intentional culture of 10x bets

Recently, I onboarded to Niyo’s Forex debit card and it helped me understand the principles of building a great product strategy by uncovering what they did so well within two aspects of their product - onboarding & driving first transaction.

In traditional mobile marketing, Businesses spend a lot of cash on all facets of customer funnel from Brand ads(awareness), downloads(performance marketing), retargeting(hey, you abandoned the cart!!) and deep activation(performance marketing for CPX events, where X is the event of interest). Niyo seemed to have short circuited its way to product led growth by compelling user centricity for latent, but meaningful problems. It was as if, someone cared so users wouldn’t have to suffer and then sit through the sitcoms of ads for their JBTD, because that was what average PM’s usually ship an app for.

This may make you laugh, but most of PM’s are in denial when users use the product in a different reality than the PM’s version of JBTD/user stories. which is why, Niyo exceeded my expectations on user centricity on these counts.

This post is my attempt to use Niyo as a usecase to framework’ize my thinking on this topic.

From my previous posts, you may have noticed my obsession for deep product led thinking for changing customer needs/preferences - to think about not just “what is”, but “where does it need to go”.

Instead of tearing up your product(again) in two quarters, you can take it there today, widening the gap for the next best alternative in your market’s mind. I also obsess over “what doesn’t work” in everyday products I use from the lens of a customer and these tear downs give me the perspective to spot delight, find ways to re-create it while thinking at a “full basket of attention” from a user’s lens.

In this post in I will connect the dots between 3 topics -

Ask your developer - Jeff Lawson(CEO, Twilio) on how to build better software

Competing Against Time - George Stalk on what you don’t innovate today essentially accrues its interest from the future

Niyo’s strategy on onboarding and what I think are meaningful ways for it to compete upwards in the value chain and develop its own playbook to become a Super-app and full blown neo-bank(and product differentiation in banking)

First, the backdrop & framework

Circa 2011, Marc Andreessen wrote the classical "software is eating the world", which is a framework for building high-growth, high-margin & highly defensible businesses, as the information asymmetry/opaque price markets flatten out and only two forms of differentiation stay - cost(cheaper, better, faster) or value(materially different understanding of needs & inbound innovation cycles) advantage.

While fortunes are made at beginning in all opaque markets, the gains almost never last unless both cost & value innovation legs co-evolve. This was the case in crypto markets, when many price loopholes across markets were exploited by SBF earlier in FTX’s journey across Japan and US, purely on arbitrage and its collapse in 2022(incl. other orthogonal reasons).

The companies who really got the “We are a tech company” have been living it much earlier than 2011. Consider Amazon 2004, when Jeff remarked - “Our business is not what is in those brown boxes, it is the software that sends the brown boxes their way” and the notion that it “Amazon is not a retailer, but a software company”. Such is the clarity that vertical defining companies get about their business and then scale that thinking in their Org through its culture of customer obsession.

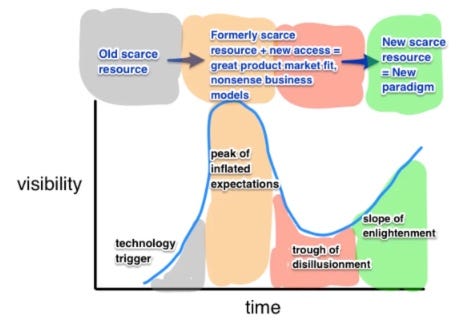

Why technology matters for vertical businesses and how the market prices them ?

Technology makes disruption of business models possible, elastic and predictable.

Consider this. In 2019, seven “biggest techs” exceeded $8 trillion dollars(market cap) with almost double the market cap of the top 200 banks. The big techs traded with price-to-book ratios above 5.0 during 2019, while banks have been stuck in the price-to-book range of 0.8 to 1.2 for much of the last decade.

Revenues are made at a point of friction where resources are scarce - money, time, access, convenience are exchanged for a premium. Incumbents guard the scarce resource as much as they can because that’s how they make money. New technologies remove that friction by giving a new access to the scarce resource and that’s how incumbents get disrupted - Alex Danco

Time and again comes an innovator that using tech adds a muscle of scaling that was never before possible. It creates an asymmetrical paradigm shift in risk-reward equation & elasticity. Let this sink in for what it means for capital efficiency in traditional business vs its asset light software counterparts.

Mind set to manifesting right to win in any industry

(…and some lessons from 2016-2017’s Ad tech armageddon)

Summary :

Mindset #1 : Turning “on or off” software infra - building an infinite capacity of serve customers

Mindset #2 : Programmable nature of “on or off” software for ignored market segments. Who you choose to serve matters. ( != always serving an underdog segment)

Mindset #3 : People & operations in the software are the weakest link to infinite scaling

Mindset #4 : An intentional product metric culture that doesn’t over-optimize for individual PM’s narrow window of success and brings 10x bets to foreground

Mindset #1 : When any business of delivering brown boxes, becomes like AWS - it can turn on or off its “software infra”, with infinite capacity of serve its customers with negligible incremental(better still, declining) cost to serve. This becomes an unbounded business that can then focus on abstracting what kind of brown boxes can it move through that value chain.

Mindset #2 : Mindset #1 doesn’t just mean building micro-services or modularity in your software, but how closely your software can truly run autonomously 24/7 and generate cash for its stakeholders(Airbnb and Marriott example above that negates large working capital needs, with handsome ROI that public markets reward) . The more software can mimic the nature of capital, being “on or off” - without people, the programmable nature of software - the more defensible its business. This differentiation is hard to copy for a long amount of time - just like the concept of HUB in Sam Walton’s initial thesis of Walmart’s focus on small towns(against unconventional wisdom of serving cities with large populations, or downtown retail districts) or the Netflix’s customer obsession on back of its data troves. This unlocks a new, previously ignored wedge and builds a massive empire which can bring vastly superior cost advantages to the conventional markets later, by which time the incumbents have been made irrelevant. The same playbook was used by Salesforce against Siebel that ignored the SMB market for CRM in 1999.

Mindset #3 : If a business needs to add substantial manpower to scale, it is just a digitally enabled business, that will see the bloodbath in more extreme business conditions. Back in 2017, when I was with InMobi, Adtech industry was facing massive headwinds(popularly known as ad tech armageddon), consolidation. Majority of businesses were running with “Take rate” as the currency of (cost)differentiation. It was bad for the whole industry.

Rocketfuel was acquired by Sizmek that year(2017) and there were many bloodbaths for operational people and a shift from ad network to becoming a true Tech company. (Sizmek itself was acquired by Amazon in 2019).

Case in point - companies that obsess to alleviate operational expenses to build cost invariant ways to scale, truly achieve the Amazon’s flywheel at global scale. Rest just exist dragging in obscurity with occasional shimmers of greatness to which it may not have yet earned the right to win.

Mindset #4 : A lot of companies have a north star metric(s), but do not use a “so what” in these metric to drive conversations with it as a focal point for where it its product focus is. The difference in aspiration vs reality is the intentionality of this focus. It becomes like a painting in the living room that appeals cosmetically to the spirit of patron’s exploration, but nothing that motivates them enough to pack their bags and set out to explore.

An intentional product metrics culture will remind everyone in all micro interactions why you put the painting in the first place. If you gloss over the metrics, the user has no seat at the table, or Amazon’s metaphorical “empty chair in the room”. You will still make a lot of good business decisions, but will loose the symphony/intentionality of working backwards, and doing it resourcefully on behalf of the user.

Worse yet, fast shipped features will even make this situation worser as each Product owner would only optimize for their narrow window of success. Why ? Enter Conway's law.

Conway's law and that most 10x bets will get “worse first”

Any organization that designs a system will produce a design whose structure is a copy of the organization's communication structure. — Melvin E. Conway

The same is true all products that grow beyond a point, where the entire product metric doesn’t fit in a coherent view in every single product owner’s view, or sometimes even the product leader. This is not just a product culture failure, but also wrong tradeoffs initially guarded as harmless things.

This makes product more away from the real metric we seek to truly optimize. Any meaningful process may even make a few product metrics worse first, but good product owners will know which direction the product is going.

Rule of thumb on what is not (intentional) worse first culture

Adding more complexity

Adding more operational sidebars

Teaching user new mental models for that use case

A lot of weight gets thrown behind cranking MVP out, unintentionally lower the baseline for exception product design & execution. Strong product leaders know to call the bluff and empower the teams to make these tradeoffs, without having to punch it all on their shoulders(authority card)

The complexity in all user facing experiences should be invisible and that is the true swag of a great product Leader. The business goals should be thought to the level of depth, where it can be no longer made simpler, and the cultural acceptance that it is every product owner’s business to know how the user experiences the entire company, even multi-suite products, even if the user only uses one product today.

Great product leaders = Chess players they are able to hold a very long window of product’s evolution in their mind, are able to make everyone see & feel the moves with limited information they know today about the market.

Bad product leaders = Do not think of simplicity as an end goal. As a result of this, metrics are changed midway(if they were there to begin with). Product breaks at seams all the time, with the business becoming a feature factory. Output, but not outcomes.

Discovering the conviction for 10x product bets

(…Moving from good to great)

10x product bets feel like going to gym - it can take substantial time, before the end user will see end result. But the craft of a great product owner is to have a compelling version of MVP’s not just to keep up momentum, but also drive consistent exceptional execution.

A good example from one of my previous experiences at Sharechat comes to mind here. Sharechat is a product much like Facebook feed and we relied on user’s explicit signals such as like, share, favourite, comment, download and popping out a content. Since users consumed a lot of content, but only “explicitly engaged with a handful” - this meant that we were neither capturing not using ~95-99% of personalisation signals to drive user retention. To put this in perspective, most of our user retention(end outcome metric) experiments were in 0.1% points improvement, if +ve at all. Input metrics were larger.

This meant that we had maxed out our levers. The 10x bet was to instrument dwell time - that is the time a user actually consumes a post. Pause for a moment. Think about consuming LinkedIn feed, do you pause and read some content more than others ? Do you go back to it, just after casually snacking that content ? This was one of the working backwards project that I lead.

What this meant was actually instrumenting the dwell time set of signals reliably. Putting the app adoption cycles(30+ days to even get ~10-15% core traffic adopt it) into play, and you can imagine, how a product owner starts to see a self constrained friction that go beyond “appraisal cycles”.

This limits high conviction 10x bets in most orgs, because no one gets fired for picking IBM and staying in safe turfs is probabilistically more rewarding. The public/ private market just doesn’t punish the layers at the org enough to bring innovating on a 10x bet into the present.

No one gets fired for picking IBM - building an intentional culture of 10x bets

The reality of 10x product bets : things that are far out/structural pieces will not get done, if you don’t have a right Product leader for the job.

Most organisations only reward building, not re-building unless the metrics speak for themselves, and unintentionally end up building a culture of “no one gets fired for picking IBM”. This manifests in becoming 1% worser every day, and you are only left with 36.6% of where you started a year back. Take this journey for an average product owner’s tenure of 2-3 years, and they metaphorically destroy most value they inherited.

It’s your bloody job as a product owner to question and speak what no one else will and do the hard things, about the hard things :) This is why obsession matters, while not compromising on execution speed.

What you say no to, is as important as what you say yes to. Your no’s are about focus, your values, what you can/will put on the line, while you create a psychologically safe environment for your much Jr team that can’t yet see the entire picture, but doesn’t have to run to you for every micro decision and to spend cycles on alignment on what next to do, second guessing their own autonomy . They know their focus on “hands on, eyes on and minds on”, better still without you in loop, autonomously.

In internal multi functional, multi stakeholder meetings, your inner conviction to not change the stance depending on who is asking - gives other’s courage. You mostly change your opinion basis new information about business constraints, realities and it’s users needs with too few exceptions. Consistency then becomes guiding principles on what should your team do, too.

Finally, my experience with Niyo and uncovering its product strategy

2 weeks back, I used Niyo to get a forex (debit) card( with Equitas bank) and I noticed the product followed the happy path on most of these frameworks and basis this, I am inferring what it’s product culture could be. This section will appeal to Product folks who want to understand how to create intentional conditions to build delightful experiences in margin enhancing ways.

And if you are from Niyo’s team - take a bow !!

Unmet user needs and working backwards

The trigger point for me : I had to take a 2x expensive international trip(Japan) with family. Unlike the previous arrangements, where I whip out an excel working backwards from estimated per day expenses, with cash & forex, and then the logistics of procuring it, I wanted a digital first experience, while feeling confident and in control of the entire process.

Primary need : Since Japan is expensive, have a margin for error to under-plan the forex in native currency - but also the confidence that I can instantly spend, transparently. Basically, the benefit of Credit card without the sticker price effect of true post transaction price.

Ability to track the expenses without all the counting/collecting/digitising/ keeping track of invoices while travelling

Transparency of what is the effective price per transaction so we on on track and in budget as a family and use this to enforce shared financial discipline goals)

After return needs :

ZERO/minimal expense reconciliation after return

ZERO/minimal sending emails to banker to “return the unused forex” back in bank (and, the paper work on this !!)

Non goals : Collecting reward points, I value simplicity, and invisible products. I just-don’t-have-the-time to do mindless discovery. While I experiment with products because it makes me a better product leader :)

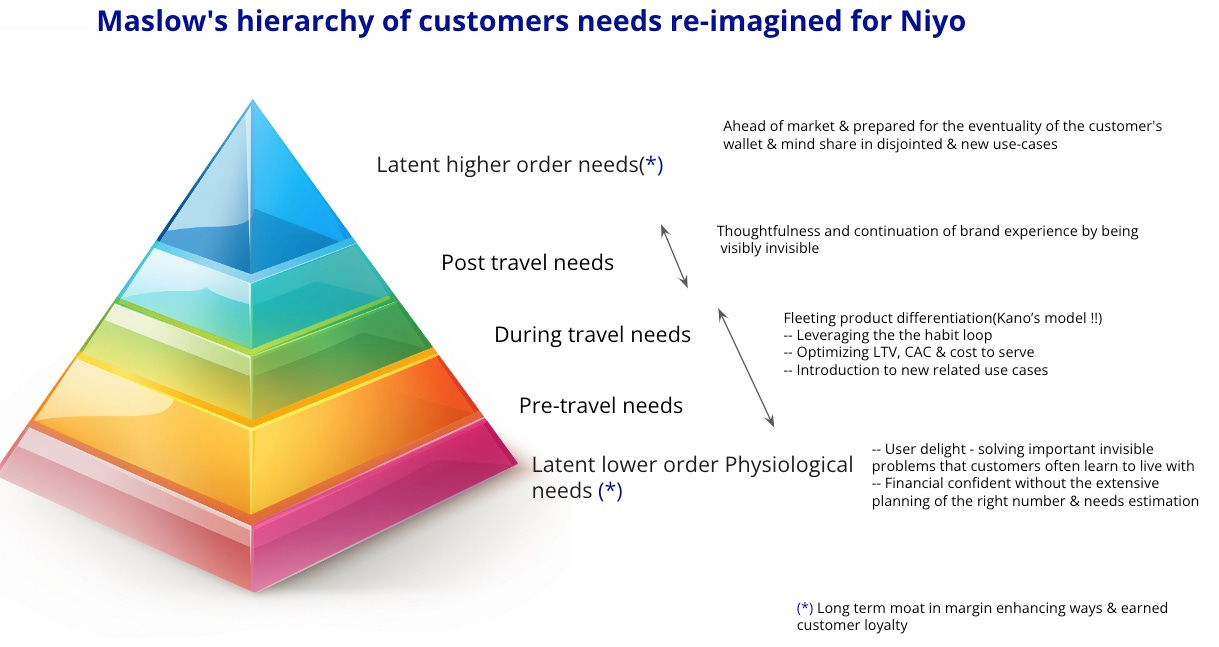

A funny thing I tell the teams I have led is that a PM thinks of product needs like these unmet needs user stories but a user rarely every writes down what they need. Our version of RICE (Reach, importance, confidence and engg effort) will only be a directional estimate - and our only guard against these to understand the layers of needs, much like Masclow’s hierarchy of needs.

Niyo’s 10x delightful onboarding - Magic moments !!

The Product - First of all in a world where everyone is trying to sell you buy now, pay later or credit related products, a debit card product re-applied intelligently to forex usecase is fresh. Customers understand both the Debit card and forex card and the product is cross between the two - with an instantaneous aha moment - I don’t have to over-plan !! Zero forex markup is also a good premise, but is less tested, basis how often bank sell zero cost products as Zero EMI products, making the purchase actually more expensive and getting people in consumer debt when in-fact waiting out could be a better option for most consumers, if not for mis-selling.

Niyo’s beauty : Meeting the psychological need of not having to plan with precision, alleviating the the fear of being stranded on foreign shores, the bitter taste of selling bills post trip, afterwords.

It’s not the actual amount lost on selling back, but the anticipation of loss. This is what makes consumers irrational on needs, making decisions emotionally and the paradox of choice.

I say intelligently because forex cards were meant to be pre-loaded debit cards, except that today most of them are static. Reloading them is incredibly painful(with GST + convenience charges every-time you reload the card and ~12-24-48 hours delay load time), withdrawing left over-in card currency painful(emailing to your banker, following up, margin and slippage on selling and the bitter taste of loss aversion ), and harrowing experience of running out of cash when abroad - nothing matches that fear.

I absolutely loved the thought process to onboarding and it did not feel like "onboarding was fragmented" into a bunch of PM's - which is usually the case in most orgs as some product cultures tend to over optimise just a PM’s own set of narrow metrics. And onboarding is the top of funnel and the most impactful experience a user has with the brand.

The most delightful part of onboarding was the live KYC. I logged in via my mobile number, key’ed in my Aadhaar, and it did an online identity identification(which triangulates address basis self declaration later). The experience preps me up gradually into a live video call with an agent, all during the same session. Just before this, it solved the most critical part of onboarding - capturing documents !!

In my previous onboarding experience with Zerodha, the KYC was prompted to hold a OTP on a sheet of paper(this ensures fidelity of actual user doing the verification and removed odds of impersonation). While Niyo could have also done this on auto pilot, this (live) man in loop step, establishes the comfort while “signing online, live in call” and permissioned mode of doing so, with a quick human onboarding touch. My estimate is operationally it may take Niyo 25-40 INR per live KYC call - which they may effortlessly put on autonomous auto pilot once Niyo reaches full scale network effects(and organic pull). Put this 25-40 INR in perspective to most ad campaigns, time duration of targeting, and you see the margin room in CAC.

The onboarding, gets my PAN card, which it uploads during the call and a live video signature - the hidden beauty of which is that short-circuits a key problem when a customer does an online in app "sign". Traditionally, the online sign rarely matches the one in "real physical world"(fat fingers). Niyo inverted this problem on its head, and even made it cheap from engineering standpoint(just the right engineering), repurposing video call and screenshot for capturing this.

But the real magic was what happened behind the scenes. For perspective I was struggling with a UPI id(to transfer funds) on a IDFC bank account I created ~2 months back, and Niyo got the deep integration so UPI just linked it right after the call (Equitas bank) - I can imagine this is not only deep thinking, but also not stopping at the lower bar since "well there is no better baseline of other banks and we are at 10x already". My guess is that Niyo may save Mn’s of dollars for not having to retarget/nudge users to complete onboarding as a function of this experience, while lowering the time to onboard, when the product is so fresh in Customer’s mind.

The layers of delight & magic in one onboarding flow is hard to not notice.

The Product strategy and the flow reminds me of bunq's freshness on an old space - banking delivered digitally. Niyo also has a bunch of new tricks which often are overlooked in mobile apps, eg : all the follow up actions had deep in app dynamic links, which took you straight to that ONE thing it wanted you to do in that session. One, not 10. It was like delight, dripping in every micro interaction you had with the product.

When you start to look at Niyo not as a forex card/ travel company, but as a superapp will clever hacks to customer segmentation by 1st party data that it can then sell both financial and other products to, as it evolves. See the common thread of Swiggy/ Deliveroo/Instamart, all building their own CDP. Think of it as an actually useful cousin of CRED :) Given its multi product stack, its clear that its where its headed, too.

On transaction side(for Forex card) - it is critical for Niyo to get the user to actually add a meaningful amount in-app, and nudges the user to get (time, socially & emotionally) invested in the platform by setting your upcoming travel details(dates & purpose). This, I think is clever at multiple levels.

It tells Niyo what (will) happen in the physical world, in the absence of definite data points - ie did the customer only load the debit card as a caution / secondary instrument to carry along, or felt confident to rely on that as a primary Forex. If no meaningful successful transactions go through on foreign land, it gives Niyo a macro view of the card network and user’s operational challenges in real time and work on enhancing it.

Since Niyo needs your location to be turned on all the time while using the app, it knows where you are physically and if you end up making no reasonable purchase in this window, it can model your LTV and product interventions/targeting/segmentation very differently. If it some point, it wanted to build its own CDP/ first party transaction data - it’s already primed up for that future.

Since travel related data spends end up being distributed across cash & one off bank issued forex cards - it is a step jump at digitising your transaction data intuitively and making it actually useful. Even if a traditional bank wanted to fo this, culturally it will never be able to use its first party data for CDP use cases. So it has a moat by not having that baggage, regulation & scrutiny. Think BharatPe’s model of underwriting loans.

As opposed to most apps targeting you for the duration of lifetime, if Niyo wanted to, it can send contextual messages in your declared travel window which will drive you through the habit loop multiple times over. Remember how UPI id replaced the act of pulling out a debit cards. It is building a mid way to teach you a new pattern, while linked to the UPI, since it understands you may not use this bank as primary bank and move meaningful cash to it. If it can deliver, it can take international hyper location based in app targeting affiliate business to another level.

It of-course can also do fraud detection, risk analytics very differently in this declared window. And if it wanted it’s contact center to be truly user centric - its response for payments failure would be very different if you were not in your home country(Queue prioritisation)

Since international travel is discretionary & luxury spends, Niyo can build a deep segmentation of its customer’s spending habits, preferences, psychometrics and demographics - the top tier high value customers that every one wants :) So, it is building an intentional customer base for a low frequency use-case(How many times do you travel internationally in an year vs the number of times you use UPI app in a day ? ), that can start to build a more wholistic picture of you.

Why is having this data for Travel/international use-cases powerful ? Look at the share of UPI volume per day volume of Makemy trip(only ~0.04 Mn per day) and Go-ibibo(0.01 Mn per day) to the UPI eco-system and the story of the margin enhancing moats & new business models becomes evidently clear. Its the same model, Razor pay doesn’t make money on ttransactions but on selling data usecases. Same is the case with Twilio’s contact Center product, flex .

The road ahead for Niyo

While Niyo has multiple products around Neobanking - Niyo Global, NiyoX, Niyo Money, Niyo Bharat, Niyo Digital SA, Niyo Students Card, Niyox Salary Account - the wedge on international travel as an entry point is the strongest. Here is my take on 4 bets it could take, basis a limited outside window to their world. It may need a mix of lobbing and Tech sandboxing(bet 4) to make it happen, but as with all 10X bets of future, the wins are clear.

Bet #1 : Become the VISA king of the forex - not for arbitrage but for user base

The user mental framework that Niyo is in a position to break with Tech is the mindset of “carrying cash” internationally, from domestic shores. As opposed to current alternative of delivering cash/bills physically to the customer(through an on-ground partner N/W) - Niyo can partner with the host country to build the “recharge anywhere model” that India pioneered.

To do this, it can reuse its hub(lounge) locator - give a service fees to on-ground cash dispensing partner - and become the VISA king of the forex, effectively short circuiting a few players in the n/w and keeping a larger share of the exchange/arbitrage fees. This removes the need to hold and manage risky forex in a politically unstable world, on-ground people required to service it, and all the hassles of note circulation, fake currency etc. By digitising the physical cash rails, it can make it programmable and on demand, thus the scaling the brown boxes infinitely as their move through its system.

Bet #2 : Truly dissolve the difference between credit & debit card

Customer tranches are created unequal.

After the RBI credit card regulation in Oct 2022, a lot of international credit card transactions and online commerce standing instructions started failing. This needed an over haul from merchants to update their payment integrations for new compliance that also affected how card information was stored. This is a problem of the user group that Niyo has and by making the card invariant and invisible for the merchants, it can become an accepting merchant of choice at ePOS.

Niyo’s take on international credit is to book an FD for access to international (credit) spends. To the user, it looks like the 2-3.5% forex markup they are not paying while travelling internationally, AND also earning interest on FD (which serves as a collateral). Niyo is able to do this, since they now remove the need to bear any risk to underwrite credit worthiness(remember they still may not have linked salary accounts for most customers and not the long window of credit data), effectively making the self selection of premium customers easier.

Just like Zerodha did with its 199 INR annual maintenance fees in the discount broking space vs Upstox that ended up with a lower quality tranche of demat customers(Cost sensitive student and young adults that do not have LTV enough to justify CAC and offset the discount broking for healthy cash margins at user level.

Bet #3 : Drive financial well being with social like features, and prudent individual planning

Because of it’s digital first delivery, Niyo can mimic how users think about their relationship with money, becoming the digital equivalent of an earmarked piggy bank, with differential time based goals. It can run one of kind experiments like - saving for a trip you want to take by putting aside a pre-determined amount locked in a virtual goal-based fixed deposit (Think companies like Jar, Tortoise but for a mid-premium tier of Niyo’s users), or have user’s socials contribute towards their goals(eg : Friends & family contributing to an international honeymoon trip, which traditionally is the 1st international trip that most of middle class Indian take). This benefits the bank since the cash will now be held for a longer amount of time vs immediate the UPI based transactions to capture pre and during travel positioning and deepens the cardinality of transactions, length and quality relationship with Niyo’s banking partners. The flywheel, will also beef up Niyo’s own bank partner network.

Bet #4 : Innovation to become a financial infrastructure company. Think Stripe, Twilio, or CAMS.

Niyo money, which targets the mutual funds, stocks segment(& EPFO tracking) - badly needs a seed to bootstrap the fragmentation that consumers are fighting over for it to not be a toy app in presence of established players like Zerodha in the market. Personally I do not think that it can be the top 5 player in this segment unless it finds an ignored wedge (International stocks - but how many people really care about it, given the complex LRS investing laws and those that do, are not individuals but investing via defined instruments or sectoral fund houses)

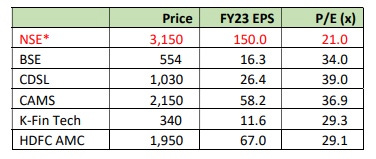

The problem of money today is its nature of fragmentation - it is overwhelming. We invest, spend, but tagging only tells what happens when the money is spent, not a state machine polling the state of machine continuously. Consider this - imagine Niyo’s premium customer makes a transaction to a stock broker or a mutual fund. By an altered payload, Niyo can choose to perpetually track the current state of money. An old way of solving this would be integration with most partners (Smallcase, Zerodha, Angelone, Groww, Upstox, HDFC Mutual fund you get the point) - instead it can LEAD can develop a protocol that sends the money, with a token to have the right to poll it, when needed. The token itself expires, and is one time use only, but enables Niyo to get an unlimited window to user’s (read only) finances in a permissioned way when initiated next by customer. A similar way of this would be to become a new age CAMS, a financial infrastructure company.

As of June’23, CAMS was running at a higher P/E multiple(36.9 than HDFC AMC, BSE and NSE which are infinitely elastic exchanges and so you see the point back home on the seven “biggest techs” exceeded $8 trillion dollars(market cap), almost double the market cap of the top 200 banks.

This is the story I wish Niyo executes, and I look forward to the neo in Niyo :)

Till next time !!

PPS : I have only covered the pre-trip experience in this post and will update this post trip on the actual product feedback incl coverage, my fitment for primary user needs, and new delighters if any.